There’s nothing like the second year of an MBA program. Although I’m taking a full 15 credit course load, I had a ton of leeway in choosing my schedule and decided to stack all my classes on Mondays and Tuesdays. With a “5-day weekend”, I plan to dedicate quite a bit of time in honing a business idea my Dad and I have been tinkering with.

As a quick recap, I learned to code this summer and for my final project I built a prototype of an online marketplace. It’s by no means a finished product, but it is a product that I can demo to prospective customers. With my 5-day weekend, I decided to fly down to Panama – the initial target market – where I attended a tradeshow. In just a few days, I’ve gained a lot of insight into both the market and the customer.

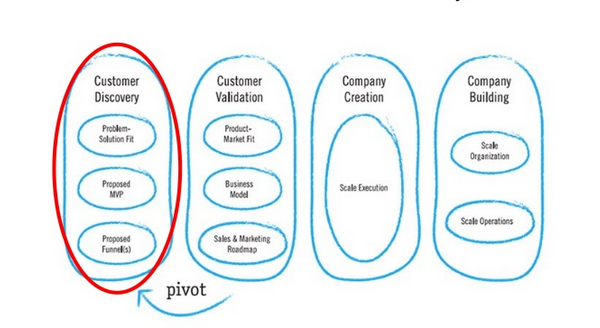

There are a lot of ways to define a startup, but the best definition I’ve found is the one proposed by entrepreneurship guru Steve Blank: “A startup is an organization formed to search for a repeatable and scalable business model.” In essence, a startup is a set of well-formulated – and therefore testable – hypotheses that the entrepreneur must either validate or debunk. With every customer insight, the entrepreneur then tweaks the business model to reflect and ultimately solve the real needs of the market. It’s an iterative process, but constantly adjusting to arrive at product-market fit is how you build a scalable business without investing huge amounts of capital upfront.

During the few days here, I spoke with a lot of people in the “vertical” my Dad and I are targeting. Three interviews with domain experts where incredibly insightful. I had a set of 10 questions that I felt would lead to a lot of insight. Although I never went through all 10, I was able to touch upon key elements that will help refine the marketplace going forward. In particular, I gained deep insight into the following:

Customer discovery: buying and selling in this market is prohibitively expensive and incredibly inefficient. I now have estimates of how much it costs to the prospective seller using the current solutions, and even how much it costs – in time and money – when a sale is unsuccessful.

Market size and market dynamic: talking with several experts, I was able to triangulate an estimate of how many potential customers exist and what the total gross merchandise value of the marketplace could be. I also learned much more about what drives sales cycle and sales channels in this industry. Most importantly, even though this is a relatively small market, I believe there are enough players to create initial liquidity in the marketplace.

Competitive landscape: I was able to piece together a pretty comprehensive map of online players and their limited solutions, as well as more traditional brokers and dealers. There are a lot of relatively small players, which leads me to believe that the supply side of the market is very fragmented. A verticalized marketplace could very well add a lot of value, not just by reducing search costs but also my reducing transaction costs.

I also learned that a key challenge of building this business in Panama will be changing the mindset of potential customers that transacting online is a viable and much better option than existing solutions. Nonetheless, the heat and vibrancy throughout Panama was intoxicating, and I am convinced that this is an optimal market to launch a Latin American startup.